Stablecoins in KSA: What a Riyal-Backed Token Could Look Like

As I was reading about SWIFT's announcement that its blockchain-based shared ledger is now live, with 17 banks across six continents piloting tokenized deposits for 24/7 cross-border payments, a question kept surfacing in my mind: if the world's biggest banking network is moving this fast, what happens when Saudi Arabia issues its own regulated stablecoin, and who actually does what? Between SAMA, CMA, licensed banks, and the global players already dominating this space, the architecture is more layered than most headlines let on.

What Is a Stablecoin?

A stablecoin is a digital token pegged to a stable asset, typically a fiat currency like the US dollar, designed to hold a fixed value while moving at the speed of a digital transaction. Unlike bitcoin or ether, whose prices swing on supply, demand, and sentiment, a stablecoin's value is anchored to something steady, most commonly cash and short-term government debt held in reserve. This is what allows it to combine the settlement speed of crypto with the price stability of traditional money, making it usable for everyday payments, remittances, and trading without the volatility risk.

One technical nuance worth flagging early: a stablecoin only needs to live on a cryptographically secured distributed ledger. Most run on public blockchains like Ethereum or Solana, but that is not a strict requirement; some, including the infrastructure central banks are piloting, run on custom, non-blockchain DLT instead. That distinction matters more than it sounds once we get to how Saudi Arabia might build this.

Stablecoins have moved from a crypto-trading tool to genuine financial infrastructure. The total stablecoin market surpassed $320 billion in April 2026, according to DefiLlama data, and stablecoins now account for roughly 75% of total crypto trading volume. That scale is why central banks, not just exchanges, are paying attention.

The Economic Structure: Who Does What

A stablecoin only works if every token in circulation is matched by real value sitting somewhere safe. That requires a division of labor between several parties, and in a regulated system, a central bank or market regulator sits at the center of it.

The Issuer

The issuer is the entity that actually mints and burns the tokens. This can be a bank, a fintech, or a dedicated stablecoin company, but under any serious regulatory regime, it must be licensed. The issuer's core job is to take in fiat currency, mint an equivalent amount of tokens, and hold the incoming cash in reserve rather than lending it out or investing it in anything risky.

The Reserve

The reserve is the backbone of trust. It typically consists of cash and highly liquid, short-term government securities, held in segregated accounts separate from the issuer's own operating funds. The reserve must always be worth at least as much as the tokens in circulation, and regulators increasingly require monthly attestations or independent audits to prove it. Under the US GENIUS Act, signed into law in July 2025, eligible reserves are explicitly limited to cash, insured bank deposits, and US Treasury bills with a remaining maturity of 93 days or less, and issuers are barred from commingling reserve funds with their own capital.

The Regulator

This is where the central bank or market authority comes in, and its role differs depending on the jurisdiction. In the US under the GENIUS Act, only licensed Permitted Payment Stablecoin Issuers may issue a payment stablecoin, and federal regulators set capital, liquidity, and operational standards. In the UAE, the Central Bank of the UAEruns this function directly through its Payment Token Services Regulation, which took effect in 2024 and requires every stablecoin issuer to obtain CBUAE approval and maintain 100% reserve backing in segregated accounts. The regulator does not hold the reserve itself, but it sets the rules for who can issue, how reserves must be verified, and what happens if an issuer fails.

The Network

Once minted, the token needs somewhere to live and move. That is the blockchain layer, public networks like Ethereum or Solana, or increasingly, permissioned ledgers that regulators can monitor more closely. The network handles settlement, the actual transfer of tokens between wallets, in seconds rather than days.

Global Players and Market Setters

Tether's USDT remains the dominant force, holding roughly 58% of the stablecoin market with a market capitalization north of $185 billion as of early 2026. Circle's USDC sits second, with about $78 billion in circulation, and it has grown faster than USDT for two consecutive years, largely because it is built for regulatory compliance from the ground up: full cash and US Treasury backing, monthly attestations, and a French MiCA license that lets it operate across the EU.

That split, between Tether's liquidity dominance and Circle's compliance-first positioning, is becoming the defining tension in the industry. The GENIUS Act formalized this in the US by requiring any foreign issuer serving American users to either obtain a US banking license or partner with one, which puts pressure on Tether's domestic strategy while playing directly into Circle's hands. Meanwhile, regional regulators are setting their own standards. The EU's MiCA framework, Hong Kong's Stablecoins Ordinance, and the UAE's PTSR all require licensed issuance and full reserve backing, signaling that the era of stablecoins operating in a regulatory gray zone is closing fast.

Ripple is worth a separate mention here. Its stablecoin RLUSD is redeemable 1:1 in US dollars and was purpose-built to plug into Ripple's existing payments network, RippleNet, and its XRP Ledger infrastructure, positioning it less as a retail product and more as settlement plumbing for banks doing cross-border transfers.

Is Proof of Reserves Actually Required?

Not in the strict sense most people assume. "Proof of reserves" usually conjures a cryptographic, real-time verification, a Merkle tree proof that lets anyone check the books on-chain at any moment. That is not what any major regulator currently mandates. What the GENIUS Act, MiCA, and the UAE's PTSR actually require is closer to traditional accounting: monthly reserve composition reports, reviewed by a registered public accounting firm, with issuers above a size threshold (currently $50 billion, which only catches Tether and Circle) required to publish full annual audited financial statements under GAAP and PCAOB standards. That is a meaningful step up from the voluntary attestations the industry ran on for years, but it is a periodic, accountant-reviewed snapshot, not continuous on-chain proof. True cryptographic proof of reserves remains far more common among centralized exchanges verifying customer deposits than among stablecoin issuers themselves, who still rely on attestations and on-chain wallet disclosures rather than live Merkle proofs. The distinction matters: regulation has closed the trust gap considerably, but it has not yet closed it the way the term "proof of reserves" implies.

Bringing It Home: Stablecoins in KSA

Saudi Arabia has been moving toward this space for years, just not through the front door most people expect. Back in 2019, SAMA partnered with the Central Bank of the UAEon Project Aber, a wholesale CBDC proof-of-concept for cross-border settlement between the two countries. That experiment fed directly into SAMA's 2024 decision to join the BIS-led Project mBridge as a full participant alongside the UAE, China, Thailand, and Hong Kong, a multi-CBDC platform that has now reached the minimum viable product stage. In parallel, SAMA has been running a digital riyal pilot focused on wholesale, bank-to-bank use cases, while retail crypto remains formally restricted.

The real shift came when Majed Al-Hogail, Saudi Arabia's Minister of Municipal, Rural Affairs, and Housing, confirmed at the World PropTech Summit 2025 in Riyadh that the Kingdom is developing a regulated stablecoin framework in partnership with the Capital Market Authority and SAMA. He framed it in scale terms that are hard to ignore: stablecoin market capitalization had already crossed SAR 1.125 trillion (USD 300 billion) globally, representing nearly three-quarters of all blockchain-based transactions, and crypto-and-stablecoin transaction volume tied to Saudi Arabia reached SAR 33.75 trillion over the prior year, about five times PayPal's volume and approaching Visa's global settlement capacity. That announcement matters because it signals the government is finally separating "crypto" from "stablecoin" in its own regulatory thinking, treating the latter as payment infrastructure rather than speculative trading, and explicitly benchmarking itself against Dubai, Singapore, New York, London, and Zurich, all of which already have stablecoin frameworks in place.

What Blockchain Would It Actually Run On?

This is the question every product person asks once the regulatory headlines settle, and it is the one SAMA and the CMA have stayed quietest on. No technical architecture has been published. But the Kingdom isn't building in a vacuum, and three existing signals point toward how this likely gets built.

Signal one: SAMA already prefers purpose-built private ledgers over public chains. Project mBridge, where SAMA is a full participant, deliberately avoided Ethereum, Hyperledger Fabric, and Corda after using them in earlier pilot phases. It now runs on the mBridge Ledger, a bespoke permissioned DLT built around a HotStuff-based consensus protocol, chosen specifically because it gives central banks deterministic finality and full control over who can validate. Notably, the mBridge MVP platform is EVM-compatible, meaning it can execute Ethereum-style smart contracts even though it isn't Ethereum itself. That detail matters: it tells us SAMA is comfortable with EVM tooling and developer familiarity, just not with running on a network it doesn't control.

Signal two: the region's actual stablecoin launches are split between three models, and Saudi Arabia is watching all three. The UAE, the closest comparable market, has tried each approach. AE Coin, the first CBUAE-approved dirham stablecoin, runs on its own proprietary blockchain network. Zand AED took the opposite path, launching as a multi-chain stablecoin issued natively across several public blockchains to plug straight into existing DeFi and wallet infrastructure. First Abu Dhabi Bank's DDSC sits in between: it lives on ADI Chain, a dedicated Layer 2 built by the ADI Foundation, so it inherits a public-blockchain security model while running on a chain purpose-built for this exact use case rather than a general-purpose network.

Signal three: Saudi banks are already placing their bets, and they're leaning EVM. Saudi Awwal Bank's 2025 partnership with Chainlink adopts the Cross-Chain Interoperability Protocol (CCIP) and the Chainlink Runtime Environment, both built around EVM-compatible chains, specifically to move tokenized assets and data securely between multiple blockchains rather than commit to one. Separately, Riyad Bank's fintech subsidiary Jeel partnered with Ripple to explore tokenization on the XRP Ledger, a non-EVM but purpose-built payments chain. Taken together, this tells me no single Saudi institution has settled on one chain, and the market is explicitly hedging toward interoperability rather than picking a winner.

My prediction: I expect a riyal-backed stablecoin to launch on a permissioned, EVM-compatible network, not a fully public chain like Ethereum mainnet, and not a closed proprietary ledger like AE Coin either. EVM-compatibility lowers the barrier for global exchanges, wallets, and DeFi protocols to integrate it without Saudi Arabia surrendering control over who can transact or settle. This mirrors mBridge's own design choice and gives SAMA an exit ramp to interoperate with cross-border infrastructure like mBridge and Chainlink's CCIP later, without ever opening validation to anonymous public participants.

Who the Network Members and Validators Would Be

If Saudi Arabia follows the governance model it has already used for mBridge and the digital riyal pilot, validation will not be open or anonymous. Expect a tiered structure:

SAMA, as the anchor validator. In mBridge, each founding central bank deployed its own validating node directly; I expect SAMA to do the same for a domestic riyal stablecoin, retaining ultimate authority over settlement finality and the ability to freeze or reverse transactions in extreme cases, something no public blockchain validator set would grant it.

Licensed issuing banks as permissioned nodes. The UAE's pattern, where AE Coin, Zand AED, and DDSC are each issued by a single licensed bank or bank subsidiary rather than an open consortium, suggests Saudi Arabia will license a small number of banks (Saudi Awwal Bank, Riyad Bank's Jeel, and similar institutions already running blockchain pilots are the obvious early candidates) to run nodes and mint against their own reserves, with SAMA auditing each one.

The CMA, as a compliance and reporting layer rather than a validator. Given the CMA's role is market conduct and disclosure rather than monetary settlement, I'd expect it to sit outside the validation set entirely, receiving reporting feeds rather than running infrastructure.

No public, anonymous validators. Unlike Ethereum or Solana, where anyone can run a node, I expect zero permissionless participation. This is consistent with Saudi Arabia's existing ban on retail crypto trading through financial institutions: the comfort level is with controlled, licensed infrastructure, not open networks.

My Predictions for Implementation

Based on the direction SAMA and the CMA have already signaled, and how the UAE's parallel rollout has unfolded, here is how I expect this to play out.

Joint oversight, not a single regulator. Saudi Arabia is structuring this as a shared mandate between SAMA and the CMA, much like the US splits oversight between banking regulators and the SEC's adjacent territory. Expect SAMA to own reserve backing, redemption, and monetary stability, while the CMA governs market conduct and disclosure, similar to the lines being drawn in the UAE between the CBUAE and VARA.

Bank-led issuance first, fintechs later. The UAE's playbook is instructive here. Its first approvals went to AE Coin's issuer, backed by Al Maryah Community Bank, and then to First Abu Dhabi Bank, before independent fintechs entered the space. I expect Saudi Arabia to follow the same sequencing, licensed Saudi banks issuing the first riyal-pegged stablecoin, with non-bank fintechs gaining access only after a regulatory track record is established.

A Shariah-compliance layer baked into the framework. Unlike the US or EU, Saudi regulators will need to resolve whether a stablecoin's structure, including any yield mechanism on reserve assets, satisfies Shariah principles before it gains mass retail trust. I expect any Saudi stablecoin to use Murabaha-style or fee-based reserve structures rather than interest-bearing instruments, explicitly marketed as Shariah-compliant from day one.

Wholesale first. Given that SAMA's CBDC work has stayed wholesale-only, I expect the first riyal stablecoin use cases to center on interbank settlement, trade finance, and cross-border payments tied to mBridge, with retail consumer access coming later once the regulatory perimeter is fully tested.

Vision 2030 cashless targets as the real driver. Saudi Arabia hit its 70% cashless transaction target two years early, in 2023, and has since raised the bar to 80% by 2030. A regulated stablecoin fits neatly into that infrastructure goal, less about competing with USDT and more about giving the Kingdom programmable, riyal-denominated settlement rails it fully controls.

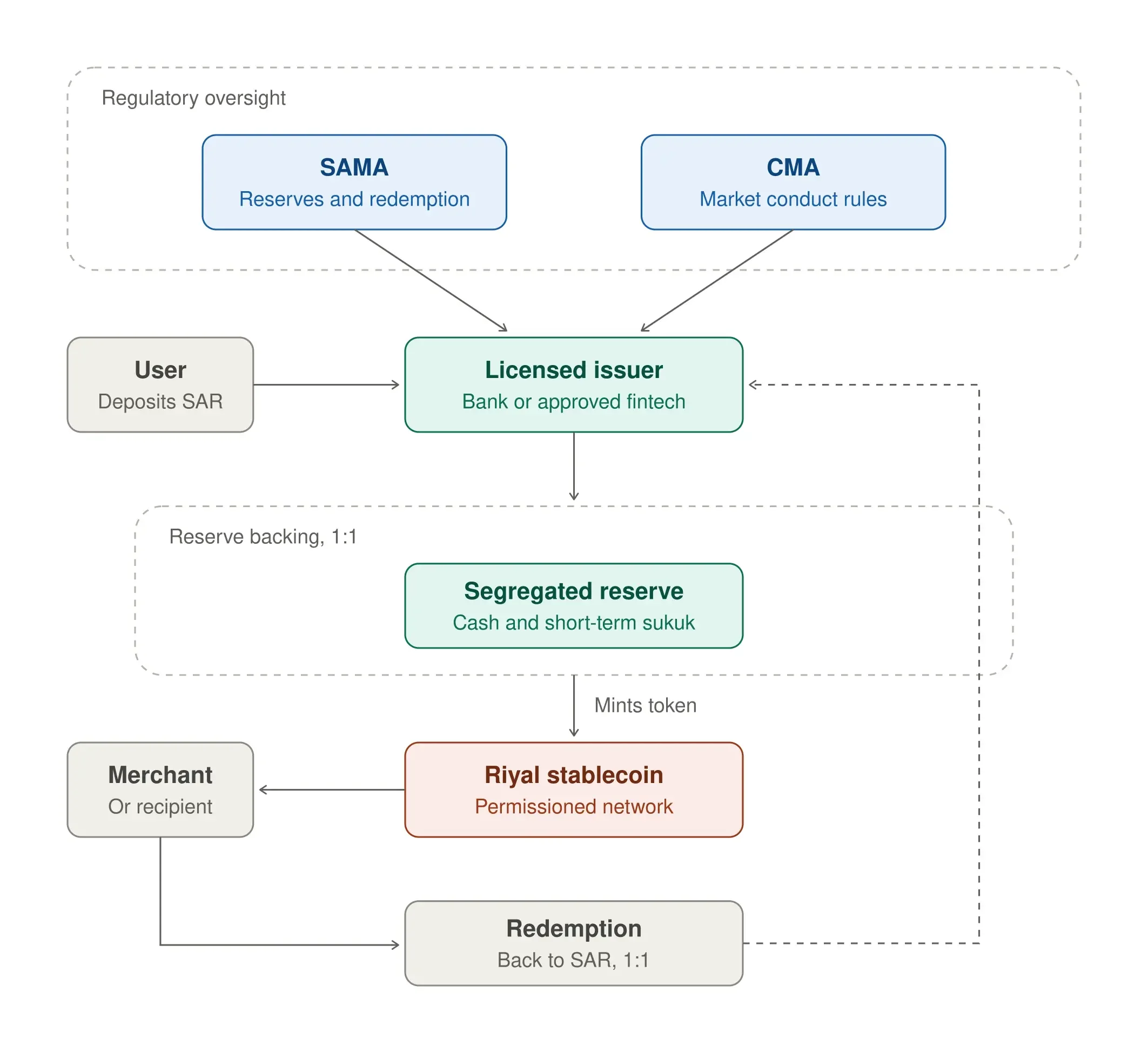

The diagram below sketches what this flow could look like once a riyal-backed stablecoin is operational:

a user funds a licensed issuer, the issuer mints tokens 1:1 against a reserve held in cash and short-term sukuk, the token moves across the permissioned network to a merchant or recipient, and it can be redeemed back to riyal at any point, all while SAMA and the CMA supervise the issuer throughout.

The diagram below sketches what this flow could look like once a riyal-backed stablecoin is operational:

a user funds a licensed issuer, the issuer mints tokens 1:1 against a reserve held in cash and short-term sukuk, the token moves across the permissioned network to a merchant or recipient, and it can be redeemed back to riyal at any point, all while SAMA and the CMA supervise the issuer throughout.

Created using Calude

The Takeaway

Stablecoins are no longer a side experiment in crypto trading; they are becoming core financial infrastructure, and the market has already chosen its early winners in USDT and USDC. Saudi Arabia is not trying to out-compete those global players. It is building its own riyal-denominated rails, on its own regulatory terms, using a structure that closely mirrors what the UAE has already proven out next door, and, if my read is right, a technology stack shaped by mBridge's own precedent: permissioned, EVM-compatible, and validated exclusively by SAMA and a short list of licensed banks. The pieces, mBridge participation, a digital riyal pilot, joint SAMA-CMA oversight, a Chainlink partnership already live at Saudi Awwal Bank, and a clear Vision 2030 cashless mandate, are all already on the board. What's left is sequencing, and based on the region's track record, that sequence is very likely wholesale first, bank-led, Shariah-compliant, and retail-ready only once the foundation has been stress-tested.

References

Stablecoins 'new foundation for global value movement': Al-Hogail. (2025, October 27). Argaam. https://www.argaam.com/en/article/articledetail/id/1852947

Swift's blockchain ledger ready for use as 17 banks set to pioneer tokenised cross-border payments on trusted global infrastructure. (2026, July 9). Swift. https://www.swift.com/news-events/press-releases/swifts-blockchain-ledger-ready-use-17-banks-set-pioneer-tokenised-cross-border-payments-trusted-global-infrastructure

Global crypto exchanges back Saudi Arabia's stablecoin, digital asset ambitions. (2025, November 6). Al Arabiya English. https://english.alarabiya.net/News/saudi-arabia/2025/11/06/global-crypto-exchanges-back-saudi-arabia-s-stablecoin-digital-asset-ambitions

Saudi Riyal Goes Digital: Inside SAMA's "Oil-Backed" CBDC Pilot. Blockchain News. https://blockchain.news/news/saudi-riyal-goes-digital-inside-samas-%22oil-backed%22-cbdc-pilot

Saudi Arabia Moves to Integrate Stablecoins, Expand Real Estate Funds. (2025, October 27). Asharq Al-Awsat. https://english.aawsat.com/business/5201905-saudi-arabia-moves-integrate-stablecoins-expand-real-estate-funds

Project mBridge reaches minimum viable product stage and invites further international participation. (2024, June 5). Bank for International Settlements. https://www.bis.org/press/p240605.htm

Project mBridge: Updates and resources. Bank for International Settlements. https://www.bis.org/about/bisih/topics/cbdc/mcbdc_bridge.htm

Zand launches UAE's first AED-backed stablecoin on public blockchain. (2025, November 17). Zawya. https://www.zawya.com/en/press-release/government-news/zand-launches-uaes-first-aed-backed-stablecoin-on-public-blockchain-osc5inog

UAE accelerates digital finance with new AED stablecoin approval for DDSC on ADI Chain. (2026, February 12). Cryptonomist. https://en.cryptonomist.ch/2026/02/12/aed-stablecoin-uae-adi-chain/

Saudi Awwal Bank partners with Chainlink to leverage CCIP and CRE in blockchain innovation pact. (2025, September 17). Cryptopolitan. https://www.cryptopolitan.com/saudi-awwal-bank-partners-with-chainlink/

Ripple Expands in Middle East with Riyad Bank Partnership. (2026, January 26). MEXC News. https://www.mexc.com/news/561057

SAMA Joins mBridge Project. (2024, June 5). Saudi Press Agency. https://spa.gov.sa/en/N2117066

UAE, Saudi central banks issue report on joint digital currency, 'Aber' project. Gulf News. https://gulfnews.com/business/banking/uae-saudi-central-banks-issue-report-on--joint-digital-currency-aber-project-1.1606654298973

Saudi Arabia fast-tracks shift to cashless economy on back of fintech boom. (2025, May 9). Arab News. https://www.arabnews.com/node/2600095/business-economy

RAKBank Receives Approval to Launch UAE Dirham-Backed Stablecoin. (2026, January 7). Brave New Coin. https://bravenewcoin.com/insights/rakbank-receives-approval-to-launch-uae-dirham-backed-stablecoin

In-Depth Virtual Currency Regulation: United Arab Emirates. (2025, November 5). Charles Russell Speechlys. https://www.charlesrussellspeechlys.com/en/insights/expert-insights/dispute-resolution/2024/in-depth-virtual-currency-regulation-uae/

Stablecoin Market Crosses $320B as Tether USDT Dominance Falls 2.5% in 2026. (2026, April 16). Bitcoin News. https://news.bitcoin.com/stablecoin-market-crosses-320b-as-tether-usdt-dominance-falls-2-5-in-2026/

Circle's USDC outpaces Tether's USDT growth for second year running. (2026, January 6). CoinDesk. https://www.coindesk.com/markets/2026/01/06/circle-s-usdc-outpaces-growth-of-tether-s-usdt-for-second-year-running

How will the GENIUS Act work in the US and impact the world? (2025, July). World Economic Forum. https://www.weforum.org/stories/2025/07/stablecoin-regulation-genius-act/

The GENIUS Act: A Comprehensive Guide to US Stablecoin Regulation. Paul Hastings LLP. https://www.paulhastings.com/insights/crypto-policy-tracker/the-genius-act-a-comprehensive-guide-to-us-stablecoin-regulation

The GENIUS Act: A Framework for U.S. Stablecoin Issuance. (2025, July). Sidley Austin LLP. https://www.sidley.com/en/insights/newsupdates/2025/07/the-genius-act-a-framework-for-us-stablecoin-issuance